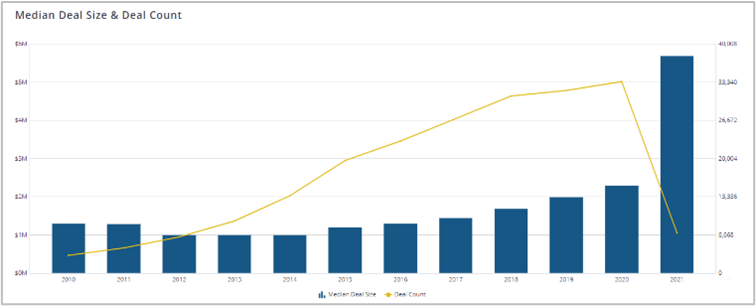

The amount of capital being invested has surged well past historical highs, and along with it have gone valuations. The median deal size in 2020 was at an all time high of roughly $2.2M, while in the first quarter of 2021, the median deal size was nearly $6M. The median post-money valuation in 2020 was $18M, and in Q1 2021 it was well north of $50M (see Pitchbook charts below).

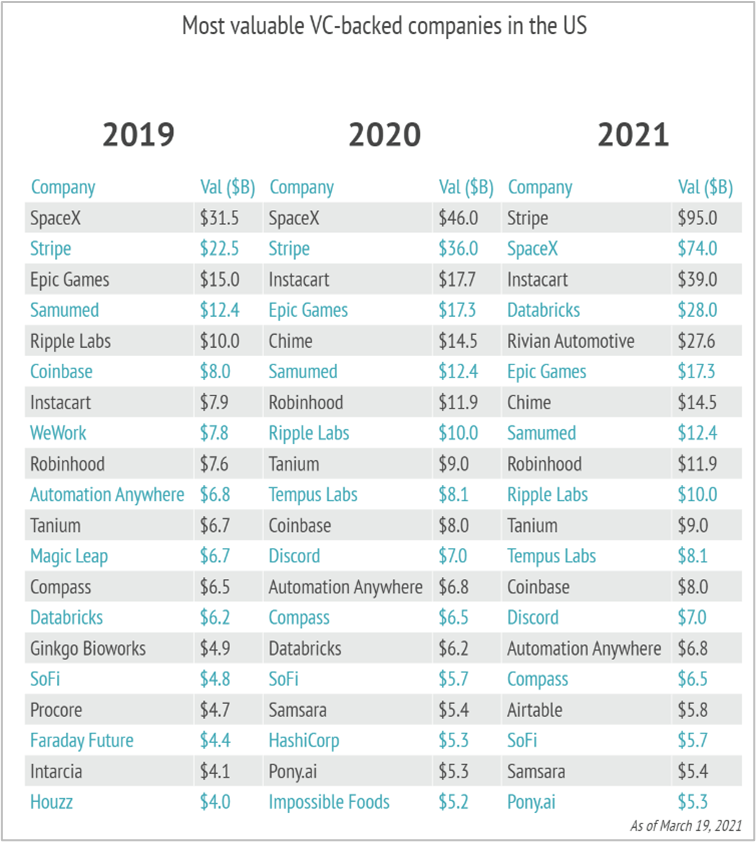

A lot of this frothiness has been the result of fintech and ecommerce companies doubling and quintupling in size over the last ~18 months (see chart on Most Valuable VC-backed companies below). This movement in digital transformation has generated mega funding rounds and massive valuations, which are dragging along the rest of the venture market. Seed and Angel investors are now demanding a higher percentage of ownership at earlier rounds to hedge against the upward pressure on valuations. This is in turn pushing Series A valuations up, and on it goes.

But, where does it end, and more importantly, when does it end?

But, where does it end, and more importantly, when does it end?

With vaccinations rolling out across most of the developed world (unfortunately, Canada is amongst the slowest) people are starting to get back to normal. We have seen bookings at CheckFront, one of our Fund holdings, start to tick up in the UK as people start booking travel again in anticipation of restrictions loosening.

Librestream, another Fund holding, experienced a nice uplift during the pandemic as companies required technology that allowed them to work remotely. In a post-COVID world, we don’t see this need for remote work tools retracting. COVID has simply accelerated the adoption of remote work technology.

Like many ‘once in a generation’ events, the pandemic has changed the way we work, live, communicate and share experiences. While the thirst to ‘return to normal’ is extremely strong in all of us, it is clear that how we define ‘normal’ has fundamentally changed.

The surge we saw in valuations of fintech and ecommerce over the last year is unlikely to unwind. Meanwhile, new types of businesses like Ghost Kitchens – restaurants with no bricks and mortar presence – will continue to emerge. We expect returning to the office will look more like co-working spaces than a traditional office setting with designated desks occupied 9-5, Monday to Friday. The impact this has had on business models and venture valuations, while perhaps not permanent, will likely linger for a while longer before things begin to settle. After all, at some point P/E ratios need to make sense.

Kristina Bergman, M.Sc.